Article Directory

The Great Mortgage Reset: Why Your Future Home Isn't Just About Rates Anymore

Alright, let's talk about the buzz, or perhaps, the lack thereof, in the mortgage market. For weeks now, we’ve watched those numbers on the screen, those crucial percentages that dictate so much of our financial lives, barely budge. They're like a highly sophisticated piece of machinery in a holding pattern, humming with fractional movements, hinting at potential, but not quite taking flight. You see the headlines, you hear the whispers—mortgage rates are essentially flatlining. And I get it, that can feel frustrating, even a little disheartening, especially if you were hoping for some dramatic plunge. But what if I told you that this apparent stagnation isn't a dead end, but a launchpad? What if the real story isn't about what the rates are, but what this steady state demands of us, the homebuyers and homeowners of tomorrow?

Decoding the Market's Whisper: Beyond the Daily Ticker

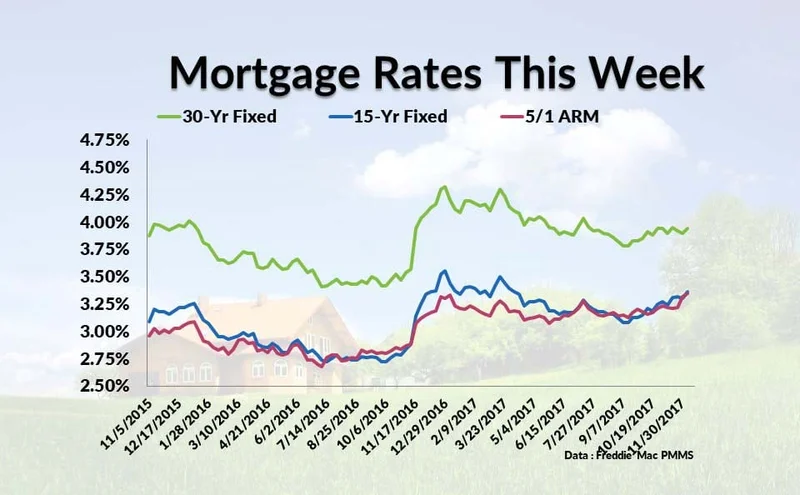

We've been glued to the screens, watching numbers like 6.244% one day, then 6.236% the next for a 30-year fixed rate. It's like watching paint dry, isn't it? But here’s where we need to zoom out. When I first saw these stable-yet-stubborn figures, particularly after the Federal Reserve started its series of quarter-percentage-point rate cuts in September and October, I honestly just sat back in my chair, speechless at the market's resilience. Many of us, myself included, anticipated a more immediate, dramatic drop. We were conditioned by the past, weren't we?

Think back to the pandemic era, that wild, unprecedented time when 30-year fixed rates dipped to an almost unbelievable 2.65% in January 2021. That wasn't just a low rate; it was a financial anomaly, a product of massive, coordinated government action to prevent economic collapse, a kind of emergency-level defibrillation for the economy. To expect those kinds of rates again, barring another global catastrophe, is like hoping for dial-up internet to make a comeback—it’s just not how the game is played anymore, and frankly, it wasn't even the historical norm. When you look at the St. Louis Fed data, rates around 7% were pretty much the standard from the 1970s through the 1990s. We've been living in a golden age of cheap money for the last 15 years, and that's skewed our perception of "normal." This isn't a return to the dark ages; it's a return to something closer to historical equilibrium, a foundational shift in how we approach housing finance, an evolution from the extraordinary to the sustainable.

Your Personal Algorithm for Homeownership: The Real Leverage

So, if we can't just wait for the market to hand us a golden ticket, what can we do? This is where the real power lies, where we move from passive observers to active strategists. The true breakthrough isn't in predicting the Fed's next move; it's in optimizing your own financial "algorithm." We're talking about taking control of the variables you can influence, the ones that matter more than ever in a stable-but-higher rate environment.

Imagine this: you're walking into a lender's office, or more likely, logging onto an online portal, and instead of just asking "What's your best rate?", you're presenting a profile that screams "low risk, high reward." That means a credit score north of 740, a debt-to-income ratio (or DTI—in simpler terms, how much of your monthly income goes to paying off debts) ideally below 36%. These aren't just arbitrary numbers; they're your leverage, your personal market advantage. Freddie Mac research tells us that just by applying to multiple lenders, you could save hundreds, even over a thousand dollars a year. That’s not pocket change; that’s real money staying in your pocket, money that adds up over the life of a loan. Are we truly leveraging every tool at our disposal, or are we still hoping for a market miracle? This isn't about waiting for a unicorn; it's about becoming the architect of your own financial destiny.

The folks feeling those "golden handcuffs"—stuck with their pandemic-era 3% rates and reluctant to move—they're facing a real challenge, but it also underscores the incredible value of what they secured. For the rest of us, it means understanding that the market isn't a casino; it's a complex system, and our best bet isn't a lucky spin, but a well-researched, meticulously planned strategy. We can't let the noise about tariffs or potential inflation, while important, distract us from the immediate, actionable steps we can take. This isn't just about rates; it's about building financial resilience, about future-proofing your homeownership dream in a dynamic world, and that, my friends, is a challenge I believe we’re all ready to embrace with open arms, because the future isn't something that just happens to us, it's something we build, brick by financial brick, together.

The Homeownership Frontier: It's All About Agency Now

Forget waiting for rates to plummet back to some mythic past. The real opportunity, the true paradigm shift, is understanding that you hold more power than you think. In this new era of steady, historically normal rates, the smartest move isn't passive anticipation; it's active, informed financial optimization. It's about taking the reins, mastering your personal finances, and becoming the hero of your own homebuying story. The future of homeownership isn't about timing the market; it's about being prepared for any market.